Why the 50-30-20 budgeting rule might not work for you

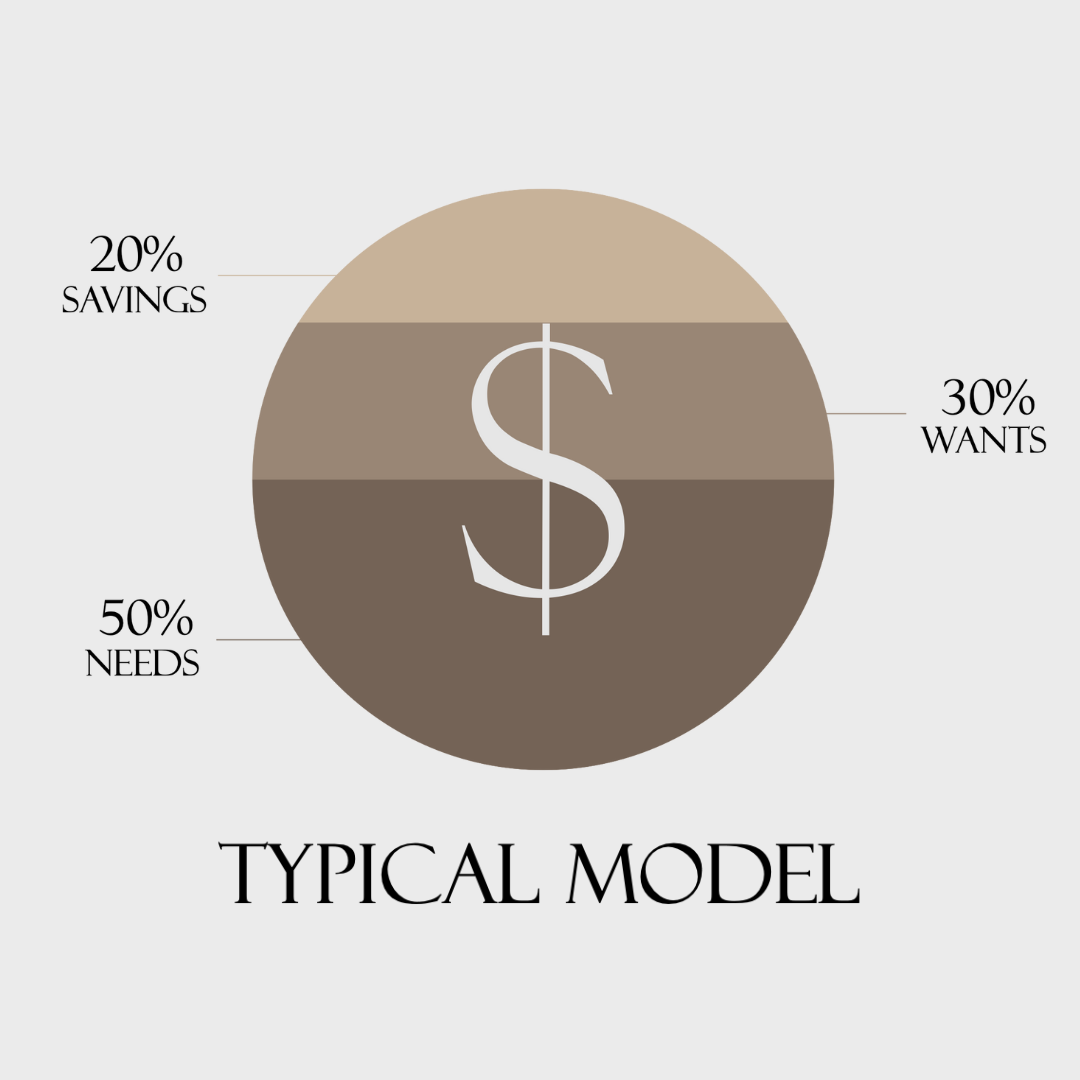

What is the 50-30-20 budgeting rule?

Chances are, if you're new to budgeting, this would be one of the first search results you get when searching for easy budgeting methods.

It's a simple and easy rule for managing your money. The basic rule of thumb is to divide your monthly after-tax income into three spending categories:

- 50% for needs

- 30% for wants and

- 20% for savings or paying off debt.

It’s great in theory but it doesn’t always work in practice and here’s why

The model does not consider your income, situation or lifestyle

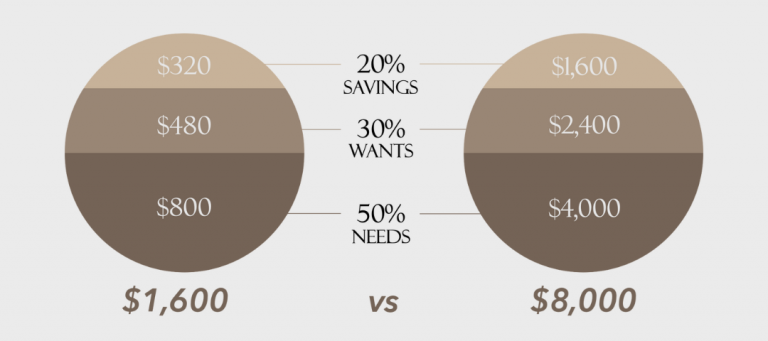

Lower income individuals might need more than 50% of their income for their needs while higher income individuals that follow this rule might end up spending a lot more than they need.

By using the examples in the chart above, we can see how a worker earning $1,600/month might struggle paying off their bills and other necessities with $800 while someone earning $8,000/month would have an excessive amount ($4,000) for their necessities.

You might also need to save more than 20% of your income to reach your goals

You might be slowed down when you have multiple savings goals or a big one like purchasing a house. This might be true for any budget, but strictly allocating only 20% of your income for savings might take you much longer to hit your goals than what you’re capable of.

How do I build a better budget then?

If you’re completely lost, using the 50-30-20 rule might be a good starting point, but you’ll have to tailor the details to your income and lifestyle.

1. Prioritise your debts

Pay off your debts starting from the highest interest-bearing to lowest. If you can, pay off your credit card bills entirely instead of just the minimum each month to avoid paying extra on interest.

2. Always pay yourself first

That means building up your retirement accounts, creating an emergency fund (about 6 months of your expenses), buying insurance and saving for your long-term goals.

After calculating how much you’d like to save each month, you’ll be able to visualise better how much you’re left to spend instead of saving as an afterthought.

Working backwards to find your savings goal

In order to reach your goals faster or budget less for savings, this is where you might want to consider allocating some of your budget towards investing to make your money work harder.

Some lower-risk investments include: high-yield savings accounts, endowment plans, divident-paying stocks and fixed annuities.

3. Use the leftover from each month for discretionary spending

If you find it frustrating to constantly track your expenses, you might want to create a separate bank account to keep these funds so you don’t confuse them with your needs or savings.

“What if I don’t have any leftover?”

You might want to look into cutting back on your savings and allow yourself some “fun” money. Getting too lost in building up your savings might cause harm to your mental health if you don’t ever get to do anything you enjoy.

More articles you might like

Is hyperinflation really coming?

(and what you can do to prepare for it) What are the factors causing inflation now? Governments pumped huge sums of money into their financial systems during the pandemic in the fo

Why the 50-30-20 budgeting rule might not work for you

What is the 50-30-20 budgeting rule? Chances are, if you’re new to budgeting, this would be one of the first search results you get when searching for easy budgeting methods.

When to know it’s time to quit your job

Have you been thinking about calling it quits at your job? There’s a lot of content out there saying “this might be your sign to resign” BUT that could be dangero

When to know it’s time to quit your job

Have you been thinking about calling it quits at your job? There’s a lot of content out there saying “this might be your sign to resign” BUT that could be dangero

Should I opt out of the Dependants’ Protection Scheme (DPS)?

What is the Dependants’ Protection Scheme (DPS)? It is a type of term life insurance: you pay a premium for a period of time (up to 65 years old) and if you pass on during th